| Year | Opening Balance (₹) | Deposit (₹) | Interest (₹) | Pension (₹) | Closing Balance (₹) |

|---|

Looking for an online EPF Calculator that helps you estimate your EPF maturity value accurately? You’ve come to the right place.

EPF (Employees’ Provident Fund) is an essential component of a private employee’s salary structure. While there is a prescribed minimum contribution rate, there is no maximum limit on how much an individual can contribute voluntarily to their EPF account.

Over the long term, EPF contributions can generate a substantial retirement corpus, thanks to disciplined savings and compound interest.

However, many employees are not fully aware of how EPF works or how to calculate the maturity amount they will receive at retirement.

This is where an EPF calculator becomes extremely useful, as it helps estimate future savings and plan finances more effectively.

EPF contributions are divided into two components:

- Provident Fund (PF) contribution

- Pension contribution (EPS)

Interest is earned only on the PF portion, while the pension contribution does not earn any interest and is used solely to provide pension benefits after retirement.

Table of Contents

What is EPF?

The Employees’ Provident Fund (EPF) is a retirement savings scheme managed by the Employees’ Provident Fund Organisation (EPFO) under the Ministry of Labour and Employment.

It is primarily applicable to employees in India in establishments with 20 or more employees, though voluntary enrollment is possible for others.

Purpose:

- Encourage long-term savings

- Provide financial security after retirement

- Offer benefits during emergencies (loan/withdrawals)

EPF Contributions

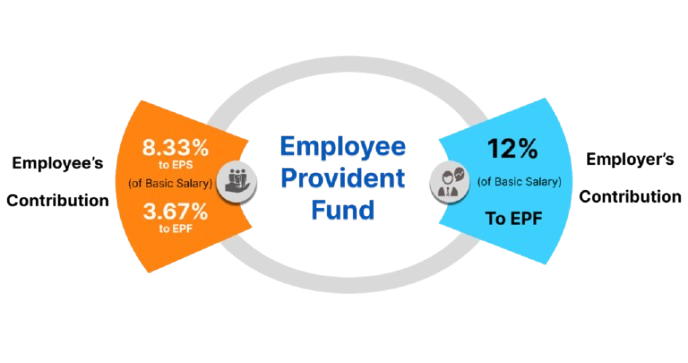

Both employee and employer contribute to the EPF monthly.

Employee Contribution:

- 12% of basic salary + dearness allowance (DA)

- Automatically deducted from salary

Employer Contribution:

- 12% of basic salary + DA

- 8.33% goes to EPS (Employee Pension Scheme)

- The remaining goes to EPF

💡 Do You Know

If your salary is above ₹15,000/month, EPS contribution is capped at ₹1,250/month.

Tax Benefits

- Contributions are tax-deductible under Section 80C of the Income Tax Act (up to ₹1.5 lakh per year).

- Interest earned and maturity amount are tax-free if EPF rules are followed.

EPF Interest Rate

- Declared yearly by EPFO (historically around 8–8.5% per annum)

- Interest is compounded annually and credited at the end of the financial year.

EPF Withdrawal Rules

| Withdrawal Category | Terms & Conditions | Amount Allowed | Typical Documents / Notes |

|---|---|---|---|

| Final PF Withdrawal (after unemployment) | After leaving a job, 75% of your PF can be withdrawn within 12 months. | Apply via the UAN portal; ensure UAN KYC (Aadhaar, PAN) is updated. | Must be unemployed for 12 months continuously before full withdrawal is allowed. |

| Immediate Access after Job Loss | Up to 75% of the total PF balance (after a minimum 25% retention applies in many cases). | Automatically enforced by the EPFO system. | No special documents if KYC is complete; application filed online. |

| Minimum Balance Rule | EPFO recommends keeping a minimum of 25% PF balance locked for retirement security. | May restrict how much is immediately withdrawable. | The pension portion often requires 36 months of continuous unemployment before full withdrawal. |

| Full Pension Withdrawal (EPS) | Apply via Form 10C on the UAN portal. | EPS component only (separate from PF). | Apply via Form 10C on UAN portal. |

| Purpose | Eligibility / Terms | Amount Allowed | Documents / Notes |

|---|---|---|---|

| Essential Needs – Illness | Minimum 12 months of service generally applies; simplified category. | Minimum service period ~12 months; can claim for self/children’s education. | No specific document required if UAN KYC updated; auto settlement likely. |

| Essential Needs – Education | Housing Needs – House purchase/construction | Withdrawable up to 10 times (increased limit under new rules). | Official receipts/fee details are sometimes asked, but often no documentary proof is required under streamlined rules. |

| Essential Needs – Marriage | Minimum service ~12 months; for marriage of self/siblings/children. | Withdrawable up to 5 times. | Proof not strictly required if UAN KYC is complete; auto-settlement improves processing time. |

| Up to ~90% of the eligible balance (employee + employer share) where applicable. | Typically, longer service may be expected (varies by scheme and case), but a new broad category simplifies the rule. | Covers unforeseen hardships, disasters, etc.; now, no reason declaration required. | Property papers or purchase/loan details may be requested in some cases, but auto settlement may apply. |

| Special Circumstances | Withdraw up to 100% of the eligible balance (subject to minimum balance retention). | Covers unforeseen hardships, disasters, etc.; now, no reason declaration is required. | No specific supporting documents; process simplified for auto settlement. |

Disclaimer: The above summary is based on the latest information available as of December 2025 and is intended for general guidance only. EPF/EPFO rules can change, and individual eligibility may vary based on factors like service history, account details, and implementation. Always consult the official EPF/EPFO website or notifications for the most accurate and updated withdrawal rules.

What Is An EPF Calculator?

The EPF calculator is an online tool to calculate the maturity amount of your EPF contribution. It considers the yearly salary hike and any contribution to VPF as well.

It is a free online tool that gives you the accurate maturity amount, considering that you have entered all the inputs correctly.

How To Use the EPF Calculator?

To use the EPF Calculator, you need to provide the following inputs

- Your age ( The calculator considers 60 years as the retirement age)

- Basic salary + DA per month

- PF contribution per month

- VPF contribution ( if any)

- Expected annual salary hike

- Current PF balance

- Current pension balance

Based on these inputs, the EPF calculator will give you the following outputs

- Maturity value at retirement

- Total EPF contribution

- Total interest earned

- Total pension amount

Benefits Of Using The EPF Calculator

- The EPF calculator considers all the possible aspects while calculating the maturity amount. So, the result you will get is 100% correct

- It considers the yearly salary hike, VPF contribution, and any current balance you have in your PF account

- The tool is free to use and for unlimited times

Conclusion: EPF Calculator

The EPF calculator is a valuable tool that helps individuals clearly understand their retirement savings and plan their financial future with confidence. By providing quick and accurate estimates of contributions, interest earned, and maturity value, it enables users to make informed decisions about saving and long-term financial goals.

Using an EPF calculator regularly encourages disciplined savings, better financial awareness, and preparedness for life after retirement, making it an essential resource for effective financial planning.